Why Restaurant Owners Are Rethinking How They Pay for Kitchen Equipment

Equipment costs are rising and margins are tighter. Here's why more restaurant owners are financing kitchen equipment instead of paying cash upfront.

Outfitting a commercial kitchen can cost anywhere from $50,000 to more than $500,000, making equipment one of the largest capital investments a restaurant owner will ever make. That range alone explains why equipment payment decisions carry more weight than they used to. That level of investment forces restaurant owners to balance immediate cash flow needs with long-term operational growth, making financing decisions as important as equipment selection itself.

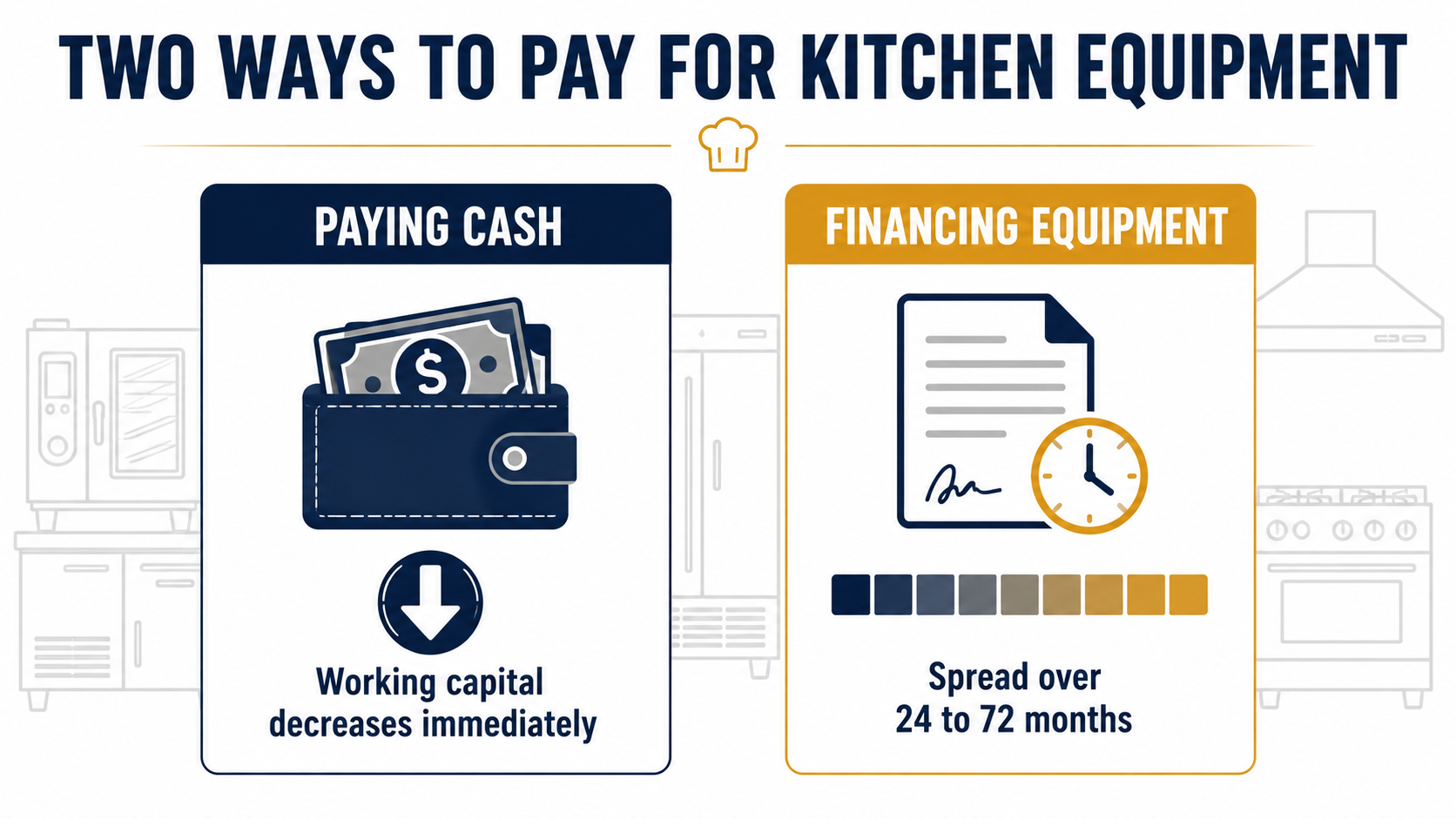

A decade ago, paying cash upfront was the default for operators who could manage it. Today, a growing share of restaurant owners are financing equipment even when they technically could pay outright, and the reasoning behind that shift says a lot about where the industry's margins actually stand.

This is not a story about restaurants being unable to afford equipment. It is a story about what owners choose to do with the cash they do have and why tying it up in a walk-in cooler or a combi oven increasingly looks like the wrong move.

Economic Shifts: Squeezed Operator Profit Margins

Rising food costs, labor pressure, and general inflation have squeezed restaurant margins for several years running, altering how operators analyze operational cash flow and profit margins on a monthly basis.

None of those pressures show signs of reversing quickly. For operators adjusting their cost baselines to mitigate macro pressures, understanding modern operator profit margins and implementing strategic cash management solutions is critical to surviving these tighter industry realities.

At the same time, the food-service equipment market itself has been expanding, with industry analysts projecting growth from roughly 4.8 billion dollars in 2025 to 10.2 billion dollars by 2035 as restaurant openings, franchise expansion, and kitchen modernization continue. According to ongoing economic data compiled in the National Restaurant Association research library, elevated operator demand and increasingly complex equipment designs have consistently pushed unit wholesale prices higher over the past decade.

Against that backdrop, keeping cash on hand for payroll, inventory, and rent has become more valuable than it used to be, simply because there is less margin for error if something goes wrong. As preserving liquidity became more important, financing naturally emerged as an increasingly attractive option for equipment purchases.

Why Equipment Financing Is Easier to Qualify For

Equipment financing has a structural advantage that other types of restaurant loans do not. Because the equipment itself secures the loan, lenders treat it as a lower risk product than general business loans, even for restaurants with limited credit history or a relatively short time in business. A restaurant that cannot easily qualify for an unsecured business loan can often still finance a $25,000 oven because the oven itself is the collateral.

Typical equipment financing rates currently run between roughly 6 and 20 percent annual percentage rate, depending on credit profile and the lender, with repayment terms commonly stretching from 24 to 72 months. Actual financing terms vary based on lender requirements, equipment type, business financials, and creditworthiness, making it worthwhile for operators to compare multiple financing offers before committing.

Tax Optimization: Leveraging 2026 Section 179 Write-offs

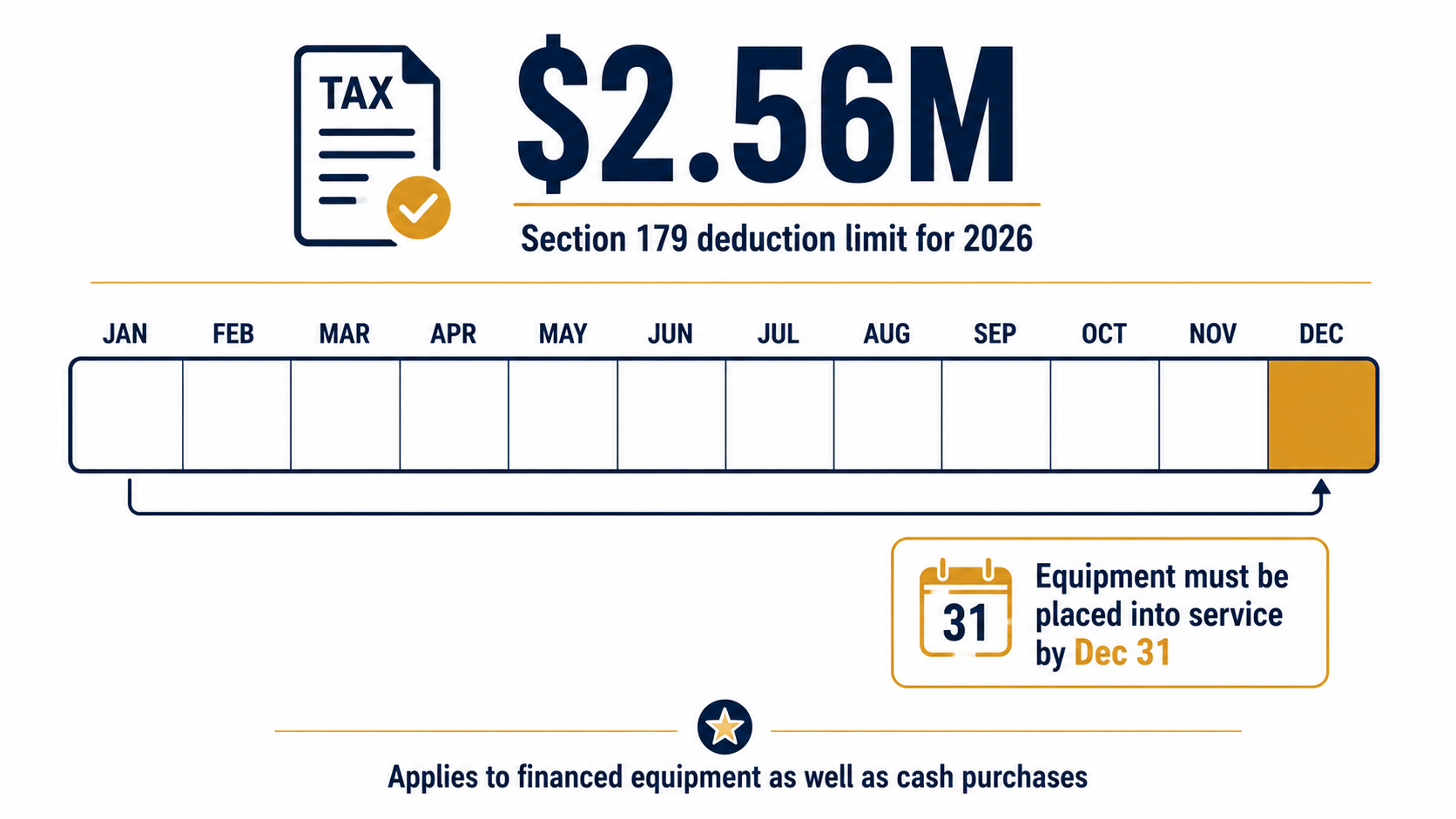

One detail that often gets missed outside of accounting circles is Section 179 of the tax code. For 2026, the tax code allows businesses to deduct up to 2.56 million dollars in qualifying equipment purchases under the official Section 179 deduction guidelines, as long as the equipment is placed into service by December 31 of that year. Financing the equipment does not disqualify it from this deduction, and in many cases the interest paid on the financing is separately deductible as well.

This means an owner who finances a piece of equipment in the spring, rather than waiting to save up cash, can both spread out the payment and capture the deduction in the same tax year, which is a combination that a slower, cash-only approach cannot match.

Capital Allocations: Asset Life Cycles and Financing Risks

Not every piece of equipment is a good financing candidate. Equipment financing works best for long-lived assets, things like ranges, ovens, and refrigeration units that will stay in service for years. Shorter-life or fast-evolving equipment, such as certain point-of-sale hardware, tends to fit leasing structures better, since the underlying technology is more likely to be replaced before a multi-year loan term is even finished.

There is also a real cost to financing that should not be glossed over. Annual percentage rates of 6 to 20 percent mean an owner is paying meaningfully more over time than a straight cash purchase would cost. The decision only makes financial sense if preserving that cash produces more value elsewhere, whether that is avoiding a cash crunch during a slow season or funding something with a faster return than the equipment itself.

How Restaurant Owners Are Financing Equipment Today

In practice, many owners are blending approaches rather than picking one method for the entire kitchen. Large, long-term assets like a walk-in cooler or a commercial range get financed over several years. Smaller, more discretionary purchases get paid in cash when the timing allows. This selective approach reflects a more deliberate approach to cash flow management than the all-cash or all-financed models that were more common in the past.

For owners planning equipment upgrades or replacements, reviewing available commercial cooking equipment options helps illustrate the types of cooking systems restaurants most commonly finance as part of long-term kitchen investments.

Conclusion

Today's restaurant owners are increasingly financing kitchen equipment not because they lack capital, but because preserving liquidity often creates greater operational flexibility. They are financing it because the math has shifted. Equipment financing offers lower qualification barriers than unsecured loans since the equipment itself acts as collateral, typical rates run from roughly 6 to 20 percent over terms of two to six years, and the 2026 Section 179 deduction allows financed equipment to still qualify for a deduction of up to 2.56 million dollars if placed into service by year end.

None of this eliminates the real cost of financing, which is why many operators are mixing financed long-term assets with cash purchases for smaller items rather than committing fully to one approach. The result is a more deliberate, cash-conscious way of equipping a kitchen than the default all-cash model that used to be standard in the industry.

Frequently asked questions

No. Many owners who could pay cash still choose to finance, since it preserves working capital for payroll, inventory, and slow periods. The decision is increasingly about cash flow strategy rather than affordability alone.

Yes. Section 179 allows financed equipment to qualify for the same deduction as cash-purchased equipment in 2026, up to 2.56 million dollars, as long as it is placed into service by December 31. Interest paid on the financing is often separately deductible as well.

Long-lived equipment like ranges, ovens, and refrigeration units tends to be the strongest fit for financing, since the multi-year loan term matches how long the equipment stays in service. Shorter-life technology, such as certain point-of-sale systems, often fits leasing structures better.

Because the equipment itself secures the loan. Lenders can repossess the financed equipment if payments stop, which lowers their risk compared to an unsecured loan, making equipment financing accessible even to restaurants with limited credit history.

Yes, in direct terms. Annual percentage rates for equipment financing typically range from about 6 to 20 percent, so the total cost over the loan term is higher than a straight cash purchase. The trade-off is preserved cash flow, which many operators value more than the lowest total cost.

Yes. Industry research suggests restaurant operators rely on equipment financing more frequently today than a decade ago, driven by rising equipment costs, tighter margins, and greater financing availability.

Research analyst at the Food Service Research Institute, covering restaurant industry intelligence and menu innovation.